Tag: insurance industry

How the insurance industry delivers service has evolved significantly in the last decade.

Regardless of what form of insurance sales or policy management your organization is engaged in, you can attest that face-to-face interactions are no longer routine and are, in fact, an oddity.

As the insurance industry’s new normal, more and more interactions between customers, industry experts, other organizations, and adjustments claims occur digitally. Though phone-based communications will continue to be a part of the customer service process for the foreseeable future, customers, care providers, other insurers, and virtually anyone else with whom an insurance company interacts have come to expect a largely digitized experience.

For any organization to thrive in the insurance industry of tomorrow, it must take steps to evolve its processes today. That means creating a cohesive modernization strategy and investing in leading-edge technology solutions.

Read more: Answering the Burning Questions of Business Leaders on Digital Transformation!

Top Challenges Facing the Insurance Industry

To understand what a modernized strategy looks like in the insurance industry, it’s vital to examine some of the top challenges businesses will face in the coming years.

1. Staffing Shortages

Historically, the insurance sector has contended with turnover rates somewhere in the range of 8-9%, according to Insurance Business America, but that span climbed to 12-15% by September 2022.

That additional turnover significantly impacts business continuity and diminishes the customer experience. It can also negatively influence insurers’ ability to replace members of leadership that are retiring or stepping away from the industry.

2. Skyrocketing Costs

Inflation and numerous other factors have contributed to rising costs of everything from healthcare to vehicles higher than ever before. Naturally, some of these cost increases are passed onto insurers and their customers, so insurance companies must find ways to absorb some of these expenses while mitigating rate increases for their clients.

Insurers should also explore ways to reduce their operating costs to keep coverage prices lower. Otherwise, businesses may find it challenging to retain customer accounts, particularly in sectors like automotive insurance, where consumers can freely shop around and change policies in six-month intervals.

3. Antiquated Legacy Systems

Some legacy systems hinder the ability of many businesses to embrace digital transformation. These aging platforms can make it challenging to comply with relevant regulatory requirements and increase an organization’s overall operating costs.

The longer that insurance companies cling to antiquated systems, the harder it will be for them to streamline traditionally tedious practices, such as claim management. Therefore, insurance companies must replace these inefficient, disjointed platforms with modern, unified alternatives.

The Role of Digital Transformation in Solving These Challenges

Digital transformation can bring modern technologies to any business process to improve its operation. Fast-growing digital transformation technologies include machine learning, artificial intelligence (like ChatGPT), customer relationship management platforms, and intelligent document processing software.

Digital transformation holds the key to solving the insurance industry’s most significant problems, and it appears that many in the industry realize this, as recent projections estimate that insurance technology spending will increase by 25% between 2022 and 2026 in the US and UK.

A cohesive digital transformation strategy will lay out a roadmap for replacing aging technologies with modern alternatives, and once these technologies have been replaced, the cost savings are almost immediate.

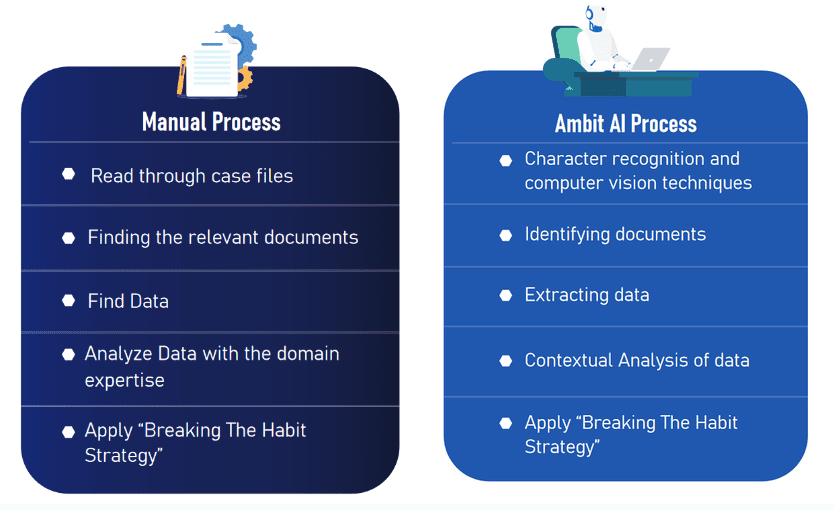

In one example of how a digital transformation strategy led to practical innovation, Fingent joined forces with the California law firm of Sapra & Navarra, LLP to develop Ambit, an AI and ML program that simplifies and enhances the management of workers’ compensation claims. Claims may include hundreds of pages consisting of a variety of letters, affidavits, forms, and other documents from claimants, doctors, lawyers, investigators, employers, and witnesses, among others. Utilizing both artificial intelligence and machine learning, the Ambit system streamlines the claims management process, reducing claim costs, and helps break the old practices of:

- Taking too long to assess claims

- Treating similar claims inconsistently

- Not equipping claim adjusters with modern tools

Instead, Ambit improves the efficiency of all parties — insurance carriers, self-insured companies, lawyers, and claim adjusters — while reducing costs for insurers by 57%.

The Ambit solution was designed to:

- Easily ingest the many documents in the claims process

- Quickly identify missing, processed & corrupted pages

- Review structured and unstructured documents automatically

- Identify areas of concern

- Suggest potential legal defenses

- Automate calculations and reminders for important legal deadlines

- Generate case summaries, with action plans

These automation capabilities not only make life easier for claims managers but enable organizational leaders to offset productivity issues created by ongoing labor shortages by reducing onboarding time for new hires. These capabilities result in more uniform handling of the claims while speeding their resolution and lowering their overall costs.

In general, automation technologies, such as those implemented during a digital transformation initiative, will also decrease operating costs, enabling insurance companies to increase their profitability and offer their customers more competitive premiums.

Read more: How AI Drives Digital Transformation In The Insurance Industry

The Essential Components of Digital Transformation

The technology trend in insurance is clearly moving from the strictly paper-based methods of the past to the digital. Beyond static websites to mobile apps. Beyond email to text and chat. Beyond processes driven by people to more and more intelligent automation that speeds up and uniformly handles all kinds of processes from marketing, and operations, to customer service.

Every organization’s digital transformation roadmap should be as unique as the business itself, but every digital transformation strategy must include a few core elements:

- Clear objectives

- An integrated plan

- A leadership-driven approach

- Investments in the right technology

When creating your organization’s digital transformation strategy, you should start by defining your “why.” In other words, you must identify the reasons you are undertaking this initiative in the first place.

From there, work with a digital transformation partner who can help you create an integrated plan that includes everyone from executive members to line-level employees.

Digital transformation efforts — even small ones — require the active support of top management. Change is the hardest thing to achieve in the organization and without the sponsorship of the corporate leaders, the effort is unlikely to succeed.

Finally, you will need to replace outdated, inefficient technology with modern, robust solutions. When appropriate,

partner with a custom software development firm that can provide you with a purpose-built solution you need for your business. They are equipped with the personnel and experience to generate a solution in the minimum timeframe and without the need to increase in-house headcounts.

If your organization has been exploring ways to improve the customer service experience, increase productivity, improve profitability, and streamline its operations, it is more than ready to embrace digital transformation.

Successfully facilitating digital transformation requires a cohesive strategy, some cutting-edge technologies, a commitment to doing things better, and the right development approach.

Read more: Digital Twin Improving Predictability and Risk Management in Insurance!

How Fingent Can Accelerate Your Process

Naturally, the cornerstone of any digital transformation initiative is technology choices. These may be an off-the-shelf system for standard processes, the integration of existing systems or, your transformation may demand a custom solution that can accommodate your business needs unlike systems available to anyone else.

At Fingent, we specialize in creating resilient custom software solutions that are able to change and adapt according to your requirements. We work with insurance industry clients to help them streamline mission-critical business processes, and – as in all our projects – we accomplish this by providing dynamic, unique software that incorporates the most appropriate technology, such as the latest in machine learning and artificial intelligence technologies.

Connect with Fingent today to accelerate your digital transformation with the help of an experienced software development partner.

Stay up to date on what's new

About the Author

Featured Blogs

Stay up to date on

what's new

Talk To Our Experts

The Growing Application of AI in Insurance Leads to a Radical Transformation

- Introduction

- Why does the insurance industry require AI now?

- What are the benefits of AI in the insurance industry?

- Top 3 primary use cases for AI in the insurance industry

- Must-have AI technologies for the insurance industry

- Are you ready to ride on the wave of AI?

Introduction

Digital transformation is not a business decision, it is a survival strategy. The Insurance industry is slowly recognizing that this vital truth is applicable to them as well. As insurers face several strategic and operational challenges due to the COVID-19 pandemic, they are recognizing that technology is the only answer and solution. Armed with this knowledge, the insurance industry is undergoing a swift and tremendous transformation, driven by the burning need to improve customer experience.

Artificial Intelligence lies at the heart of these changes and is fundamental to success. AI tries to solve the age-old problems by integrating them with existing infrastructure or by replacing legacy systems. This article answers some of the pertinent questions that will assist industry leaders in making an informed decision.

Why does the insurance industry require AI now?

Unlike many other challenges that are usually contained to one geographic location, COVID-19 is impacting essentially every corner of the world. It gave the entire planet a crash course in connected living and has made massive changes. Small insurance companies are now struggling to survive the onslaught of new requests and most larger firms may need to downsize to make it through these stressful economic times. In this climate of uncertainty, AI will be one of the key factors that will help winners survive. Until recent times, the insurance industry has only used AI in minimal ways. But there are several processes that could be improved drastically using AI.

1. Marketing and sales:

AI technologies can be used to price insurance policies more relevantly and competitively. It can be used to recommend the most beneficial products to their customers. Insurers can customize the price of their products based on individual needs and lifestyles so that their customers are happy to pay only for the coverage they need. This heightens the appeal of insurance to a wider audience while attracting some newer customers.

2. Risk management:

Neural networks of AI can be used to red flag fraud patterns and minimize fraudulent claims. AI can also be used to improve actuarial models and risks that could lead to working out more profitable products.

3. Operations:

Chatbots can be developed to understand and answer the bulk of customer queries over chat, phone calls, and email. This is especially helpful during situations like the pandemic where customers and insurers are unable to meet with each other. This can free up significant resources and time for the insurers that can be used in more profitable activities.

Read our white paper: How can your business use AI to achieve higher profits now?

What are the benefits of AI in the insurance industry?

1. Efficient process:

Currently, we are witnessing the first wave of tangible opportunities. The automation provided by AI is offering insurers reduced costing along with more efficient processes. The work dividends form the first wave of benefits. Monotonous, low-level, hazardous, and long-drawn-out tasks are taken over by machines freeing humans to do the high-level and more productive tasks. It also ensures efficiency without the margin of human error.

2. Accurately measured and priced data:

The role of underwriters is changing as AI is set to re-engineer and amplify insurance underwriting. Powered by the disruptive growth of data, AI has the potential to help underwriters analyze vast amounts of information, locate red flags, and help them make more accurate decisions. While we are not expecting to eliminate human underwriters, working alongside AI systems will ensure that all risks are accurately measured and priced.

Read more: 6 Ways Artificial Intelligence Is Driving Decision Making

3. Claims processing made easy:

Claims processing has long been a pain-point for the insurance industry. Managing claims requires a significant manual effort right from document processing to flagging potential fraud. Restricted movement during the COID-19 pandemic makes this task especially difficult. AI can be used to automate document processing. It can scan complex forms quickly and accurately. The insurance company can cut its claims processing time from weeks to just a matter of minutes. AI can help ensure that rejection of any claim is based on solid reasons. This way, insurance companies can drive cost efficiencies by reducing the number of denials that prevent claimants from going for appeals which insurance companies may ultimately have to settle.

Top 3 primary use cases for AI in the insurance industry

The advent of AI represents a quantum leap in how insurance is bought and sold, and how customers are served. Also, it is creating opportunities for insurance companies to affix their leadership positions within the industry.

Here are five primary use cases. If beginners can use this approach to disrupt the old guard, established firms can stave off new competitors and differentiate themselves from conventional foes.

Use Case 1: Always-on customer service

Insurance companies are expected to meet the customer’s expectations themselves. Gone are the days when we companies used to delegate customer service to brokers or agents. Customers expect to reach their insurance providers through any channel-like website, email, mobile app, voice call, chat, social media, etc. It’s become mandatory for insurance providers to possess multi-channel capabilities to handle queries and attend service requests. This is where AI comes to the rescue enabling insurance firms to be on the job 24/7. Always-on, multi-channel service available through chatbots, and customized interactive tools will be your secret sauce to exemplary customer service.

Read more: How AI is Redefining the Future of Customer Service

Use Case 2: Automate processes that are difficult to automate

Insurance companies employ a large workforce to manually perform operational processes. Variations in products, state-specific rules, and lack of adoptions of standards across the value chain previously made it harder to automate the process. With AI, it is now possible to predict and continuously improve the process by leveraging ML thus automating the processes effectively. By combining RPA tools with cognitive technologies, insurance companies can automate processes such as customer service requests, endorsements, and claims-processing, and provide a faster turn-around time.

Use Case 3: Continually improve the value from data

Predictive models help insurance companies determine business-critical aspects such as the maximum possible loss, probability, and pricing. However, as the companies innovate products, reach out to newer customer segments, and address new risks, these predictive models quickly get outdated making it difficult to keep up with changes. AI makes it possible to provide a feedback loop for machines to learn and adapt to ever-changing insurance business needs.

Read more: How Blockchain Enables the Insurance Industry to Tackle Data Challenges

Must-have AI technologies for the insurance industry

AI has become the cornerstone of digital transformation for the insurance industry. Leveraging AI technologies can help insurance companies address various issues that they may encounter. These are some must-have AI technologies in the insurance industry:

1. Image analytics

Insurance companies must carry out inspections to validate their decisions based on actual facts. This helps them spot any existing or potential risks and support their customers in risk management. This can be very time-consuming. The use of AI focuses on the reduction of inspection time and increases the surveyor’s productivity. It can be applied in property and casualty insurance to analyze the images of cars at the accident scene, determine the parameters, and assess replacement costs.

Advanced image analytics enables quick analysis of photos to determine parameters crucial from the perspective of life insurance. These parameters enable insurers to decide whether medical underwriting is required or not and provide an instant quote and formulate policies.

2. Internet of Things

IoT allows insurance companies to cross-sell to existing customers. They could offer discounted insurance to existing customers. There are several IoT backed devices that can detect and alert a customer when there is an issue within their home or commercial property. Integrating IoT with AI, insurance companies can offer a far superior service and enhance the customer experience.

3. Machine Learning in underwriting

The automated process eliminates the tedious and error-prone job of dealing with unstructured documents and extracts information from them to make business decisions. AI, ML, and Deep Learning can help in extracting such information, aligning it to common vocabulary, and making that information accessible through virtual assistants or search engines. This way underwriting now becomes an automated process that lasts just a few seconds.

4. End to end automation

AI helps insurers automate complex processes, end to end. Using RPA, you can tackle simpler and repeatable tasks. For example, the claims assessment process can be automated to enable the assessor to receive evidence through more advanced AI-based techniques.

Insurance companies receive data from brokers in a variety of formats and require many people to convert the data to a standard format. AI can map this data accurately allowing insurers to reduce inefficiencies in their processes. It can also improve data quality by detecting gaps and addressing those gaps in the incoming data.

Read more: Scalable Benefits of RPA in Banking, Insurance, and Logistics

5. Machine Learning for price sophistication

Price optimization techniques with the help of ML and GLMs help insurance companies to understand their customers, allows them to balance capacity with demand, and drive better conversion rates.

6. Connected claims processing

Advanced algorithms can help insurance claims to be automated which allows insurers to attain high levels of accuracy and efficiency. Data-capture technologies can replace manual methods. Evaluation of the validity of a claim is also made much simpler.

Read more: 5 Steps to Gain Business Value with AI Adoption

Are you ready to ride on the wave of AI?

Rapid advances in AI will lead to disruptive changes in the insurance industry. The winners in AI-based insurance will be those who harness the power of new technologies. Most importantly those companies who do not view disruptive technologies as a threat to their current business will thrive in the insurance industry. Get started on making sure you are one of them! Contact us to adopt the power of AI into your insurance business.

Stay up to date on what's new

About the Author

Featured Blogs

Stay up to date on

what's new