Tag: Banking

The pandemic is now the biggest and most critical challenge of traditional banking. Some of these challenges are revenue pressure, data security, customer service management, data collection and analysis, risk management, and so on. These are the warning lights and alarm bells that call for caution over emerging risks. AI (Artificial Intelligence) has gained recognition as an effective solution.

AI is empowering the banking industry to provide individualized frictionless customer experiences. It is driving customer loyalty and profitability by automating banking processes.

In this article, we will discuss how AI can resolve banking challenges. We will also discuss some of the common challenges banks might encounter in implementing AI and how a tech partner can help deploy AI better.

How AI Can Resolve Banking Challenges?

AI is the new electricity – Andrew Ng.

Modern technology such as AI can be tailored to the specific needs of the banking sector. The digital age is opening up new opportunities. According to a Business Insider research report, banks are expected to save an estimated $447 billion by 2023 with the help of AI applications. Given that, here is how AI can resolve some challenges.

Read more: Digital Transformation in Financial Services: All You Need to Know

1. AI-enabled conversational interfaces

Chatbots are one of the most popular cases of applying AI in banking. Bots are programmed to communicate with thousands of customers with minimum expense. Insider Intelligence estimates that the adoption of chatbots could save the banking sector $11 billion annually by 2023.

Mobile banking has become the most popular and chatbot services attract users’ attention and create a unique brand identity. AI functionality in mobile apps is helping banks generate more revenue than when customers visit their branches. Banking organizations that leverage AI improve their quality of services and remain competitive despite the crisis.

2. AI-enabled data collection and analysis

Banks generate an enormous amount of data every day. Collecting and recording this data is an overwhelming task for employees. Besides, all this work may be a wasted effort if there is no proper plan to use this data. Hence banks need to determine the relationship between the collected data. That is another major challenge.

AI-based apps improve the user experience by collecting and analyzing data. The collected data then can be used to grant loans or fraud detection.

3. AI-enabled Risk management

Providing loans is a challenging task for bankers. Extension of credit to a fraudster can get the bank into difficulties. Or a borrowers’ economic downturn can adversely affect the bank. 2020 statistics show that credit card delinquencies in the US alone rose by 1.4% in a duration of six months.

AI-enabled systems can appraise a customer’s credit history more accurately. Additionally, AI-powered mobile banking apps track financial transactions and analyze user data to help banks anticipate the risks associated with the extension of credit.

4. AI-powered data security

Credit card fraud is on the rise. It is the most common type of personal data theft. AI-powered systems can analyze customer behavior, location, and financial habits. So, if it detects any unusual activity, it triggers a security mechanism immediately.

Read more: Artificial Intelligence and Machine Learning: The Cyber Security Heroes Of FinTech

When all these challenges are successfully tackled, how does the AI-powered bank look like? Read on to find out.

How Does The AI-First Bank Look Like?

AI-bank rises to meet customers’ expectations and remain competitive. The AI-powered bank will offer intelligent and personalized propositions and experiences as it understands customers’ past behavior. It can span across multiple devices providing a consistent experience to its customers.

What Are The Common Challenges Banks Might Face In Implementing AI?

Implementing AI technology in banking is not always easy. You need to ensure you have the right team and expertise. You will also need access to data, resources to invest in the project, and parties that are willing to adopt the new technology.

- Access to data: It is one of the biggest challenges to implementing AI. Additionally, banks might face challenges with training data. It becomes hard to update or improve the AI models if the team does not have the necessary information to use and learn from.

- Localization: Localization is critical to the banking sector as they often need to design models with multiple markets that they serve. Localization can help you properly customize the customer experience. Your data partner can support you with localization as they have skilled linguists to develop aspects such as style guides and voice persona.

- Security and compliance: It is quite challenging to keep all the data confidential and secure. The right data partner can offer a variety of security options. They have security standards to ensure your customers’ data is securely handled. Look for data partners who have strong data protection with certifications and regulations. They will be able to provide secure annotation. They will also provide onsite service options, private cloud deployment, on-premise deployment, and so on.

- Trust, transparency, and explainability: AI models can only be successful if they can be understood and trusted by customers as they will want to be sure that their personal information is handled and stored securely. Talk to your partner and ask them to explain the model to you. Or you can always go back to the training data that was used to develop the model and extract some explainability.

- Data pipelines: Connecting data pipeline components to use siloed data is not as easy as it seems. To do this effectively, banking institutions must ensure their data is collected and structured correctly. They must also ensure that this information enables ML models to predict according to the business goals. Look for a partner with extensive security offering as their expertise will enable your banking service company to be successful and scale.

Read more: The New Untapped Opportunities for FinTech Companies in the Coming Years

How A Tech Partner Like Fingent Help Deploy AI Better?

Implementing AI into banking is a serious responsibility. It takes in-depth knowledge, an enormous amount of time, and dedication to accuracy. That is what Fingent has. We do not just follow the trends. Instead, we focus on how AI can add value to your particular banking needs.

Fingent top custom software development company, can bring transparency and explainability of AI automated decision making to your banking processes. We can provide an easy-to-use interface through APIs delivered either on-premise, in the cloud, or as a SaaS offering.

By embedding AI and ML into our products, we can accelerate the release of explainable business models that will underpin new AI use cases. These can help create a seamless customer journey and automate manual processes with self-learning capabilities. We are confident that we can help you deploy AI better. Give us a call and let’s get talking.

Stay up to date on what's new

About the Author

Featured Blogs

Stay up to date on

what's new

Talk To Our Experts

Transforming Businesses with RPA- Leading Use Cases in HR and Banking

Various organizations use RPA tools to automate simple to complex tasks and perform them with minimal or no human intervention.

From an IT perspective, you tend to bucket all RPA uses cases into data integration or testing. However, from a business perspective, you need to find out how to get a better time to value and how to overcome obstacles that hinder the business value. Then you can determine use cases that fit into this characterization.

For example, you want to roll out a change in your business process, and need integration into another system. You can do that in two ways:

- either through APIs and get into the IT changed management routine,

- or by using RPA to drive interfaces without an API and get the change rolled out in weeks instead of months.

So, time to value is the calculation that businesses need to do, and check whether the change is worth it.

Read more: What Makes a Business Process Apt for Automation

Suppose you have to perform tasks that are very repetitive in nature – like filling in excel forms, web forms, things like visual basic or word with data which you already have access to, or which you need to aggregate from various systems. Here you can have an RPA bot to pull that data or even push out that data to multiple systems. You won’t have to rekey that information manually. You can always use an RPA bot to do that in an automated fashion. In both these cases, you can write integrations or you can have a system do it for you.

RPA gives you a way to configure that behavior rather than write a code for it. In other words, RPA use cases need to be data-intensive, rule-driven, and repetitive. The drivers almost always tend to be time to value, time to market, and so on.

Now that you’ve understood where to use RPA in your business, let’s have a look at some of the use cases.

RPA Use Cases in HR

According to UiPath, 40% of your HR professionals’ time can be reclaimed using RPA. Robotic Process Automation can be combined with your existing HR systems like SAP or Workday that allows you to create digital process automation with ease. Here are the two key HR areas where automation leads to transformation.

1. Payroll:

Payroll operations consist of a large number of repetitive, rule-based tasks with activities like data collection, calculations, and scheduling tasks. Payroll workers have to collect data from various departments or units in different formats. The next step is data validation and entering that information into other applications. All these tasks are prone to error.

These activities can be automated using RPA technology since all the data that payroll staff deals with is structured. RPA can make payroll more organized without using expensive software.

The benefits of RPA in payroll are improved accuracy, lower costs due to reduced manual labor and data security. Since the number of menial, time-consuming tasks performed by employees is reduced, they can focus on tasks with higher strategic value.

2. Onboarding and offboarding:

Every time you get a new employee, the candidate’s details have to be uploaded to all systems that you use. They may need a Windows account, access to your time reporting tool, email addresses, IT equipment, and so on. If someone from the HR team manually enters all this data they would be stuck in mundane tasks. Instead, you can have a script doing these repetitive tasks. With RPA, you can automate the entire onboarding procedure since the process is the same for every new employee.

Employee exits too, have to be managed consistently. Manual processing makes these tasks error-prone and may raise auditory concerns. If RPA is implemented in this case, the bot analyzes the incident to find out which tasks need to be executed. It notifies the IT team to terminate access and recover the equipment, terminates the employee from the HCM, revokes system access, generates exit documents, and processes final payments.

Read more: Jaw-dropping Facts about Robotic Process Automation

RPA Use Cases in Banking

A slow economy and rising customer expectations have caused banks to look for cost optimization methods. The back-end processing activities in the banking sector consist of tasks that are rule-driven, repetitive, labor-intensive, and high in volume. RPA technology can help to automate these processes, thus eliminating the need for human intervention. Here are the two major banking functions that can be automated for improved results.

1. Loan application processing:

The processing of loan applications is a tedious process. For document verification, employees need to manually verify different documents and associated information and then organize all data into a single file. Very often, employees get stuck in this task and spend too much time on it. RPA employed in this procedure can automate the whole process by opening different web portals and validating the information. The bot then initiates an email to the employee for a final decision. Thus, the bot helps to save valuable time and improves the time to client response.

2. Account opening:

The account opening process is cumbersome, time-consuming, and prone to errors. RPA can help speed up this process and make it more accurate. Bots draw out information from forms and enter it into separate host applications. Thus RPA eliminates errors and improves the quality of data in the system.

Read more: How Robotic Process Automation Simplifies Business Operations

RPA tools have the potential to help various industries improve efficiency, drive faster operations, and reduce costs than most automation techniques. RPA is gaining popularity as enterprises try to counter competition, increase productivity, and meet customer expectations. Early adopters of RPA have reaped its benefits and its high time that you did too. Get in touch with our custom software development experts to learn more about how RPA can simplify your business operations.

Stay up to date on what's new

About the Author

Featured Blogs

Stay up to date on

what's new

Talk To Our Experts

Robotic Process Automation Reflecting The Banking, Insurance & Logistics Industries

Robotic Process Automation is the fastest-growing segment of the global software market. Using this technology, companies can fast-track their digital transformation initiatives. Although RPA is useful in all industries, the biggest adopters of this technology are banks, insurance companies, and logistics. These companies traditionally have numerous legacy systems and choose RPA solutions to enhance or replace manual IT processes. This article discusses how Robotic Process Automation is revolutionizing the banking, insurance, and logistics industries. First, let’s consider what is Robotic Process Automation.

What is Robotic Process Automation?

Robots have fascinated humans for a very long time. From the futuristic robot Maria from the movie Metropolis in 1927 to this day of AI sci-fi, the possibility with robots is a topic of endless discussion. Interestingly, though, this word “robot” in Robotic Process Automation (RPA) does not involve a physical or mechanical robot. Instead, it is a software running on a virtual or physical machine. Aaron Bultman, director of Product at Nintex simplified the expression saying, “RPA is a form of business process automation that allows anyone to define a set of instructions for a robot or ‘bot’ to perform.”

How to accelerate your business growth with Robotic Process Automation

According to Gartner, RPA grew by 63% in 2018 and continues to be one of the fast-growing technologies in many industries! RPA lets companies automate current tasks as if a real person was doing them across systems and applications. It interacts with each system just as a human user would interact. This does not require complex system integration. These functional RPAs are virtual workers and execute rule-based information processes, enhancing efficiency and accuracy. Additionally, it is easy to model and deploy. Let us consider the three specific industries where RPA is most beneficial.

RPA in Banking

The banking industry is completely process-oriented. Every activity is done meticulously to avoid errors in processing. The repetitive nature of the job and the high probability of human error could cause mistakes that might prove very costly. Therefore, in the recent past, leading banking institutions have started using RPA to minimize errors. According to a report by KPMG, RPA will perform almost 75% of the existing offshore jobs, which could save operational cost.

Scalable Benefits of RPA in the Banking Industry

- Mortgage Lending. RPA can enable the banking industry to meet loan quality and cost concerns head-on. Automation of repetitive and time-consuming manual tasks will free up your team to focus on the more important details of loan applications. It speeds up the work, increases revenue. enhances customer experience, reduces operational costs, decreases risk and improves compliance.

- Compliance and Risk Management. It enables the banking industry to automatically integrate and aggregate compliance information into business processes, streamlining the required work while reducing expenses. RPA eliminates the need for manual regulatory monitoring and data collection. It can empower risk management and compliance teams. It enables banking industries to avoid costly fines and damages to reputation. It provides accurate and complete information.

- Customer Service and Support. RPA ensures the longevity and loyalty of your customer relationship and the future of your bank. It helps you engage customers in real-time. It automates customer service activities so the customer is not waiting endlessly. It increases the productivity and efficiency of the team.

Related Reading: Check out these 5 simple hacks on using banking mobile apps safely.

RPA in Insurance

An insurance company receives hundreds of claim requests. Validating each request and handling them is not only a herculean task but also a painstakingly slow manual process. The entire process of the claim takes several days. Because this is a costly and time-consuming process, the company risks losing customers. To prevent further damages, insurance companies are now relying on RPA to help them improve operational excellence and reduce costs.

Scalable Benefits of RPA in the Insurance Industry

- Improves customer service because RPA effectively reduces the turnaround time in resolving customer issues.

- Processes and workflows could be tracked and recorded at each phase. This reduces staff workloads and improves process efficiency.

- Reduces the processing time by 40-80%. This frees up the team to focus on more important activities such as acquiring new clients.

- Reduces errors made during data entry significantly.

- Speeds up and organizes the processing of claims through a systematic underwriting process.

- Based on the demand, intelligent bots can scale up or down, which delivers consistency in service and operational efficiencies.

- Improves audibility and operational risk management due to the accuracy level of RPA.

- The time for the cancellation process could be reduced by one-third.

Related Reading: Here’s how machine learning is accelerating paperless offices for legal firms.

RPA in Logistics

The logistics industry depends on several processes to facilitate the proper distribution of products, materials, and services from B2B or B2C. The need for an intelligent logistics system increases as the industry along with competition advances every day. Here’s how the RPA can contribute to the logistics industry:

Scalable Benefits of RPA in Logistics.

- Better data management and customer service. Negative experiences and a multitude of errors with logistics providers are causing customers to lose their trust in online shopping. With the benefits of automation and digitalization brought about by RPA, logistics providers no-longer need to rely on huge amounts of paperwork, which was the underlying cause for errors and poor customer service. Logistics companies are enabled to manage real-time monitoring of flow and resources, availability, costs, staffing, transportation, suppliers and so on more efficiently.

- Improved work safety for employees. Through the use of automated machines in unsafe environments and the reduction of repetitive stress in manual tasks, work injury has been dropping steadily with the aid of RPA. This results in savings in terms of injury compensation and loss in reputation. It can also increase productivity, improve employee satisfaction and loyalty, and increase their efficiency.

- Improved efficiency and precision. RPA can help logistics companies easily manage the supply chain processes more efficiently. The anticipatory logistics system helps companies gauge the demand from their customers and adjust their production volume accordingly. It can help in managing and analyzing huge amounts of data within seconds, resulting in fewer human errors, faster deliveries, and fewer errors in delivery.

- Cost reduction. Fewer errors from human decision-making result in cost savings for logistics companies. Also, RPA reduces the need for human workers, which results in fewer paychecks and more profits. Where workers are still needed, it can raise their productivity, margins to a whole new level. It improves customer satisfaction and creates a safer work environment for the workers.

Related Reading: Know more about how AI is reshaping the supply chain and logistics industry.

Empower Your Business With RPA

According to Global Market Insights Inc., the RPA market is expected to reach $5 billion by 2024. It is increasing capabilities and improving performance while reducing costs in several industries. Fingent Technologies has been one of the top software companies empowering industries globally with robotic process automation capabilities. Give us a call and let us discuss how we can transform your business with RPA.

Stay up to date on what's new

About the Author

Featured Blogs

Stay up to date on

what's new

Talk To Our Experts

There were times when common banking activities like withdrawal of money or deposit of money meant time-consuming visits to the bank and waiting in line for hours. As inconvenient and troublesome as that was, it also meant less risk of being cheated and less chances of theft of personal information. Today, we have banking at our fingertips, with mobile banking applications. What we used to do in probably three to four hours earlier, can be done now with a few simple clicks or taps in a matter of seconds and that too from anywhere in the world if you have a smart device and the internet. But how secure are these mobile banking apps and online transactions? Could someone be stealing all the information you send out through such apps?

The truth is that there are various risks of being victims to such cyber attacks, but thankfully mobile banking apps these days are made with several layers of protection and it would take considerable effort for a thief to break in through all of that. Nevertheless, there are some things that you should do too, to make sure that your information is safe and protected while using mobile banking apps. Here’s what you should do for a safe banking experience online:

- Avoid following links and thus phishing – Phishing refers to the practice of acquiring personal and important information such as passwords, usernames and the like by pretending to be a trustworthy person or entity. It basically involves tricking someone into providing sensitive information and then using that information for malicious practices. It is in a way similar to actual ‘fishing’ as both of them involve bait to lure the victim into the trap. The bait in phishing could be a simple text message with an internet link or an email, or even a website, which could even look like your bank’s website (spoofing). You should never follow links on such emails and messages. According to the Federal Trade Commission, these are the most common ways that scammers use to steal private information from you. Legitimate companies and banks never ask for credit or debit card numbers, passwords or social security numbers and the like through emails and texts, so if you see a message somewhat like this:

“We suspect an unauthorized transaction on your account. To ensure that your account is not compromised, please click the link below and confirm your identity.”

DO NOT click on the link. - Download only the official banking app from a reputed site or store – Most leading banks offer their official applications on most smartphone app stores. For a fact, such apps are a lot more safe and secure than other apps and are definitely better than sending SMSs and emails. Banks actually go a long way to ensure that any information entered and sent across through their apps is encrypted. Hence make sure you download only the official app and only from leading well-known app marketplaces, like that of Google’s and Apple’s. Your bank will probably have information about their official app on their website, which you can use to verify the credibility of the app you are about to download.

- Avoid banking through public networks – Public WiFi networks are often not that secure. Even simple banking activities like checking your balance can make your private information vulnerable over the network. Most places that offer such WiFi or hotspot networks often advise their users not to share private information through it. It is always better to switch to your phone’s network in case you have to use your banking app while in a public network, as fraudsters and thieves could also be using the same network and may be waiting to steal your information. Some phones allow automatic switching to WiFi once they are in range of an open one. Hence, make sure you are not on a public network before using online banking apps or sharing any private, sensitive data.

- Avoid having personal data on your phone – For the same reason that your phone is the most convenient tool that you can easily carry around everywhere, it also proves to be sort of a risk sometimes. Your phone can have all kinds of information, like your calendar appointments, your passwords and your contacts. Such information can be read by other apps and other devices if not properly monitored and can be used against you. It also means you should be careful about where you leave your phone. Try avoiding maintaining private information on your phone as much as possible. If at all you have to, make sure you have several layers of protection for your phone. This will at least give you some time to lock your phone in case it gets stolen or lost.

- Make sure you have an updated anti-virus system – Keeping your system up to date with the latest software along with the latest security patches can actually help a great deal in keeping away malicious software and people. It is also good to download an appropriate, trusted antivirus program for your phone as well. That adds as an extra layer of protection to the phone as well.

Keeping all these points in mind, you can very well use mobile banking apps safely. All you need to do is be a little careful and alert. In spite of all this, if you happen to lose your phone, you have the Federal Laws to the rescue. According to CNN, you can recover your losses with a limit of $50 if you report the loss within two days of its discovery. Several banks apparently already have policies in place, that waive the liability completely. Even then, prevention is better than cure, so it’s always better to avoid theft and follow these simple steps while using mobile banking apps.

Stay up to date on what's new

About the Author

Featured Blogs

Stay up to date on

what's new

Talk To Our Experts

Some marketing campaigns are hilarious and others heartbreaking, whatever they are, they are interruptive for sure- because it makes you stop by and notice! To justify the statement, you may think digital marketing campaigns should always be the most attractive and catchy. But that is not often the case. For instance, the banking and finance industry is one of those industries in which you cannot really make use of a lot of creativity and colorful marketing campaigns. Whether it is a social media campaign or any other kind of digital marketing technique, you need to put in a lot of thought, while also keeping in mind the various regulations governing the financial industry. So, how exactly can you go about digital marketing for this industry?

Here are some tips:

- Talking to customers about more than just banking – Whether it is through the social media or through any other digital marketing channels like e-mails or websites, it is important to keep your customers engaged. It is true that talking to customers about events and activities in the banking industry can be rather less exciting and it might be difficult to keep the customers engaged. Hence, you need to make an effort to think beyond the financial perspective of what you can do for your customers and get them talking about what they might be interested in or what they can relate to. For example, you could ask questions through your facebook page to get to know your customers’ opinions on general matters of interest like events that happened in their city etc.

- Adding a little color – When using social platforms for marketing, make sure that you talk in their language. Connect with them and communicate with them like they do. If you make your communication formal, on any social platform, it will turn out to be an extension of your website and people will lose interest. Hence, you can share pictures or videos of events in banks or of new services provided, and engage with customers in a meaningful way. For example, Wells Fargo has posted pictures of the last signs switching over through a social media channel when they transitioned the last of their Wachovia branches over, instead of sharing a press release about the same.

- Organizing contests – Contests have always proved to be one of the most effective ways to engage with customers. You can have contests on any digital marketing channel, although it might be most effective on a social networking channel. Contests, again help you connect with and keep regular contact with your customers. For example, HSBC Students had promoted their scholarship contest through social networking channels and it triggered an overwhelming response within their community.

- Highlighting success stories – What could be more effective for promotion than a genuine third party endorsement. Rather than having self promotional ads, you can have some of your existing customers share online, their experiences with your bank. You can identify some of your customers whom you’ve had the longest relationship with, or some with a unique story etc. and share them through your digital marketing channel. If you share these stories in a creative and fun way, you can have your customers interacting and engaging in no time.

These are some things you can do while carrying out your digital marketing campaigns. In order to increase the effectiveness it can be accompanied by other regular marketing campaigns as well like partnering with colleges or universities etc. Marketing for banks and financial institutions, even though is a tough job, if done properly and thoughtfully, can generate best results.

Stay up to date on what's new

About the Author

Featured Blogs

Stay up to date on

what's new

Talk To Our Experts

In 2014, we saw the banking and financial services industry in the midst of a compliance crisis. Therefore, Most banking institutions pursued a shift in focus from defensive compliance remediation to revenue growth and cost reduction. Some banks had to settle some of their mortgage-related cases, the fines for which were quite huge. Further, the banks sought to increase operational efficiency and thereby enhance their financial performance. For this, they simplified their operations and went on to even cut down on their branch network. According to a research conducted by Deloitte, the industry closed down 1614 branches over 12 months ending in June 2014, which was the biggest downturn in over 2 decades.

Now, the US economy is in a much better form compared to 2014. However, statics show a slight slow down in 2019-20, which is again forecasted to have a steady growth in the coming years.

The financial services sector has entered a new phase with a stronger focus on increasing profitability. In this post-crisis phase of improvement, banks and financial institutions are likely to focus on 7 areas in order to enhance growth and profitability. These are:

1. Achieving balance sheet efficiencies

Banks will have to revamp their deposits and assets mixes this year, so that they are in conformity with compliance regulations and at the same time do not compromise on increasing profitability. In order to retain deposits, banks will have to boost their customer relationship programs and increase cross-selling efforts. New rules regarding the Liquidity Coverage Ratio (LCR) and the Supplementary Leverage Ratio (SLR) which were finalized in 2015, will have to be complied with in this regard. Find more on Basel III Leverage Ratio Rules in this video.

All financial institutions having more than $250 billion in total consolidated assets or more than $10 billion in on-balance sheet foreign exposure are required to have a 100% LCR. In the case of assets, investments will have to be made keeping in mind the new rules of the Net Stable funding ratio.

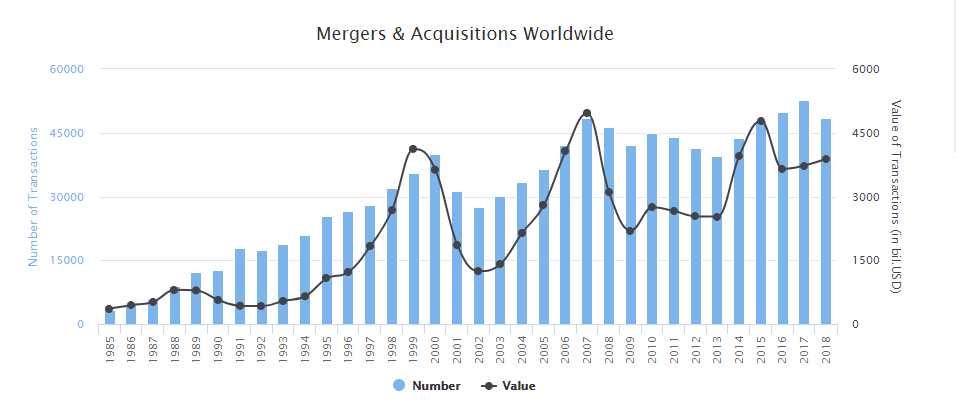

2. Driving Mergers and Acquisitions

Since 2000, more than 790’000 transactions have been announced worldwide with a known value of over 57 trillion USD. In 2018, the number of deals has decreased by 8% to about 49’000 transactions, while their value has increased by 4% to 3.8 trillion USD.  Although 2016 witnessed a dropdown, Mergers and acquisitions (M&A) are likely to continue growing in 2019, the main driving factors being efficient and strong balance sheets, challenges to the growth of revenue, limitations to achieving cost efficiencies etc. Banks, however will have to focus more on adhering to the compliance regulations concerning M&A, especially in cases where the amount exceeds $10 million or $50 million, wherein the scrutiny will be stricter.

Although 2016 witnessed a dropdown, Mergers and acquisitions (M&A) are likely to continue growing in 2019, the main driving factors being efficient and strong balance sheets, challenges to the growth of revenue, limitations to achieving cost efficiencies etc. Banks, however will have to focus more on adhering to the compliance regulations concerning M&A, especially in cases where the amount exceeds $10 million or $50 million, wherein the scrutiny will be stricter.

3. Pursuing growth

Since 2014, there have been many obstacles to growth like low demand for loan, especially mortgages. The competition has also been quite heavy especially for fee-based services like wealth management. This year, there will a stronger focus on growth. Banks will have to invest in customer analytics as well as digital technology in order to develop better cross-selling strategies and also generate more interest of the customers. But, underwriting standards should be complied with strictly. With regard to competitive advantage, establishing partnerships with non-banking technology firms could be beneficial.

4. Transforming payments

Banks have replaced their traditional cards with the EMV standard of chip and PIN cards. A Statista survey carried out in June 2018 revealed that 83 percent of Americans between 30 and 49 years owned a credit card. The total credit card debt in the United States amounted to approximately 0.83 trillion U.S. dollars in the second quarter of 2018. With the introduction of Apple Pay, contactless payments are also becoming quite popular. And as contactless payments become more accepted, banks will have to look for ways to distinguish their way of delivering customer experience.

Fun Facts: In April 2018, the four major U.S. credit card issuers — Visa, Mastercard, American Express, and Discover — decided that they’ll no longer require signatures as a verification method for purchases. Retailers may still require signatures to verify cardholder identities, however, but only if they choose to do so. This will help streamline the checkout process without compromising card security — signatures aren’t a very good security measure, and cashiers never check them anyway.

5. Strengthening compliance management

In 2014, as mentioned before, banks and financial institutions had resorted to dealing with compliance pressure by strengthening internal control and resolving existing legal and regulatory issues. Further, as the compliance regulations have been bolstered, banks need to integrate compliance and risk management fully into the culture of the banks rather than concentrating on specific processes. It should be enforced in the performance management systems as well, through employee training. New regulations like heightened risk governance expectations and the enhanced prudential supervision rule specifically require the banks to improve their risk capabilities.

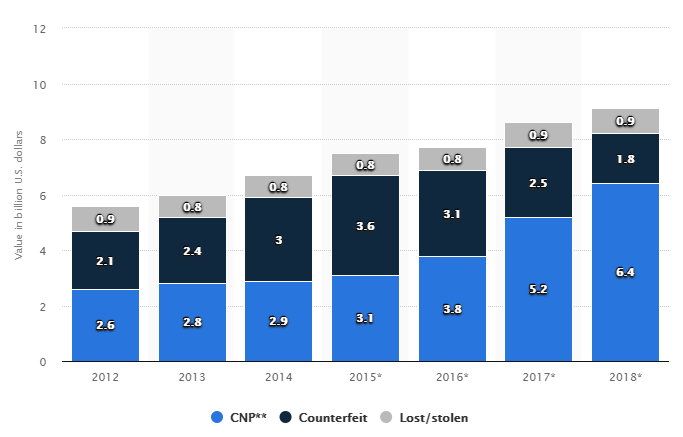

According to Statista reports, payment card losses due to counterfeit amounted to three billion U.S. Dollars in 2014 which declined to 1.8 billion U.S. Dollars in 2018.

6. Managing data and analytics

Since 2014, the efficiency of the data management processes followed in most of the banks had been found to be just about average. From a recent survey conducted by the Risk Management Association and Automated Financial Systems Inc., it was found that only 40% out of the 37 global financial institutions surveyed, felt the quality of their data to be above average or excellent. Banks now need to move toward a central Regulatory Management Office (RMO) in order to monitor the data management processes. Besides that, the Chief Data Officers should also extend their responsibilities and help in collaborating with new business lines and functional groups, which will help in value creation.

7. Enhancing cybersecurity

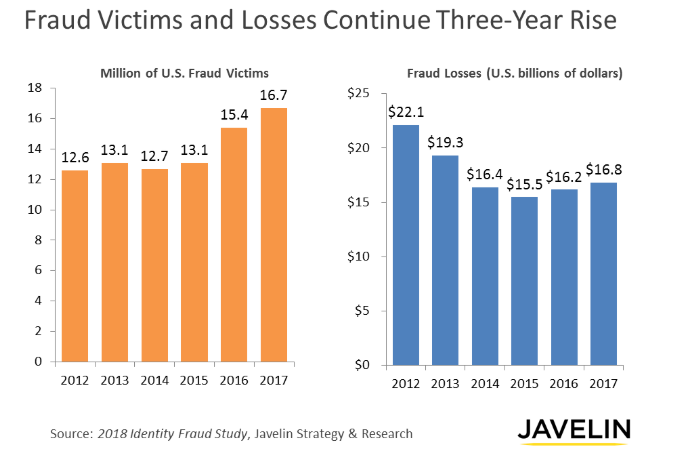

In 2014, there was a huge rise in the number and severity of cyber attacks. The 2018 Identity Fraud Study revealed that the number of identity fraud victims increased by eight percent (rising to 16.7 million U.S. consumers) in 2017, a record high since Javelin Strategy & Research began tracking identity fraud in 2003. The study found that despite industry efforts to prevent identity fraud, fraudsters successfully adapted to net 1.3 million more victims in 2017, with the amount stolen rising to $16.8 billion.

To improve cybersecurity efforts, banks are likely to add advanced features to their existing systems. New methods like Wargaming, attracting specialized talent etc. will prove to be quite helpful. Enhancing the existing intelligence systems to detect new threats or attacks on a regular basis could also be very helpful.

As the economy improves, banks need to invest more into technology for most of their concerns whether it is compliance or customer relations or cybersecurity. Improving data analytical capabilities will ensure that the ultimate goal of growth and profitability is achieved. Moreover, with ethics and risk management embedded into the organizational culture, it further assures improved profitability.

Fingent works with a number of financial institutions to help them be ahead in the market. Along with advanced technology practices, Fingent helps financial institutions implement industry proven practices to help their clients overcome challenges for growth.

Stay up to date on what's new

About the Author

Featured Blogs

Stay up to date on

what's new