Tag: Insurance companies

How the insurance industry delivers service has evolved significantly in the last decade.

Regardless of what form of insurance sales or policy management your organization is engaged in, you can attest that face-to-face interactions are no longer routine and are, in fact, an oddity.

As the insurance industry’s new normal, more and more interactions between customers, industry experts, other organizations, and adjustments claims occur digitally. Though phone-based communications will continue to be a part of the customer service process for the foreseeable future, customers, care providers, other insurers, and virtually anyone else with whom an insurance company interacts have come to expect a largely digitized experience.

For any organization to thrive in the insurance industry of tomorrow, it must take steps to evolve its processes today. That means creating a cohesive modernization strategy and investing in leading-edge technology solutions.

Read more: Answering the Burning Questions of Business Leaders on Digital Transformation!

Top Challenges Facing the Insurance Industry

To understand what a modernized strategy looks like in the insurance industry, it’s vital to examine some of the top challenges businesses will face in the coming years.

1. Staffing Shortages

Historically, the insurance sector has contended with turnover rates somewhere in the range of 8-9%, according to Insurance Business America, but that span climbed to 12-15% by September 2022.

That additional turnover significantly impacts business continuity and diminishes the customer experience. It can also negatively influence insurers’ ability to replace members of leadership that are retiring or stepping away from the industry.

2. Skyrocketing Costs

Inflation and numerous other factors have contributed to rising costs of everything from healthcare to vehicles higher than ever before. Naturally, some of these cost increases are passed onto insurers and their customers, so insurance companies must find ways to absorb some of these expenses while mitigating rate increases for their clients.

Insurers should also explore ways to reduce their operating costs to keep coverage prices lower. Otherwise, businesses may find it challenging to retain customer accounts, particularly in sectors like automotive insurance, where consumers can freely shop around and change policies in six-month intervals.

3. Antiquated Legacy Systems

Some legacy systems hinder the ability of many businesses to embrace digital transformation. These aging platforms can make it challenging to comply with relevant regulatory requirements and increase an organization’s overall operating costs.

The longer that insurance companies cling to antiquated systems, the harder it will be for them to streamline traditionally tedious practices, such as claim management. Therefore, insurance companies must replace these inefficient, disjointed platforms with modern, unified alternatives.

The Role of Digital Transformation in Solving These Challenges

Digital transformation can bring modern technologies to any business process to improve its operation. Fast-growing digital transformation technologies include machine learning, artificial intelligence (like ChatGPT), customer relationship management platforms, and intelligent document processing software.

Digital transformation holds the key to solving the insurance industry’s most significant problems, and it appears that many in the industry realize this, as recent projections estimate that insurance technology spending will increase by 25% between 2022 and 2026 in the US and UK.

A cohesive digital transformation strategy will lay out a roadmap for replacing aging technologies with modern alternatives, and once these technologies have been replaced, the cost savings are almost immediate.

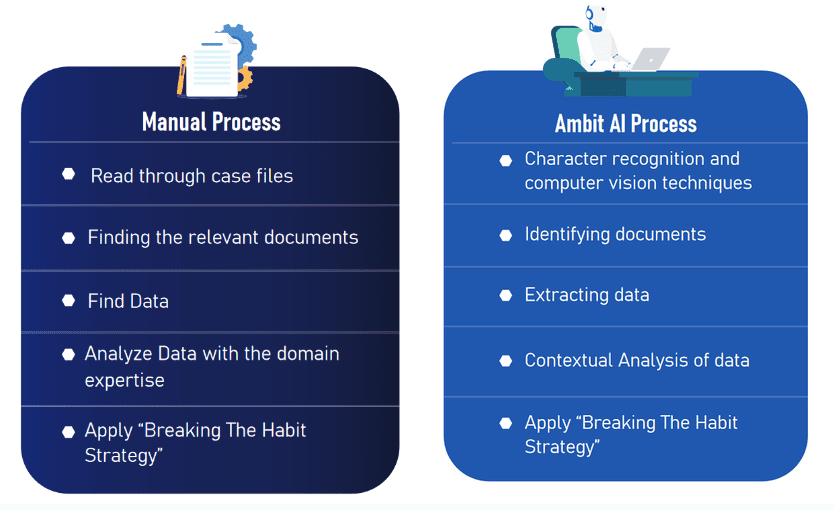

In one example of how a digital transformation strategy led to practical innovation, Fingent joined forces with the California law firm of Sapra & Navarra, LLP to develop Ambit, an AI and ML program that simplifies and enhances the management of workers’ compensation claims. Claims may include hundreds of pages consisting of a variety of letters, affidavits, forms, and other documents from claimants, doctors, lawyers, investigators, employers, and witnesses, among others. Utilizing both artificial intelligence and machine learning, the Ambit system streamlines the claims management process, reducing claim costs, and helps break the old practices of:

- Taking too long to assess claims

- Treating similar claims inconsistently

- Not equipping claim adjusters with modern tools

Instead, Ambit improves the efficiency of all parties — insurance carriers, self-insured companies, lawyers, and claim adjusters — while reducing costs for insurers by 57%.

The Ambit solution was designed to:

- Easily ingest the many documents in the claims process

- Quickly identify missing, processed & corrupted pages

- Review structured and unstructured documents automatically

- Identify areas of concern

- Suggest potential legal defenses

- Automate calculations and reminders for important legal deadlines

- Generate case summaries, with action plans

These automation capabilities not only make life easier for claims managers but enable organizational leaders to offset productivity issues created by ongoing labor shortages by reducing onboarding time for new hires. These capabilities result in more uniform handling of the claims while speeding their resolution and lowering their overall costs.

In general, automation technologies, such as those implemented during a digital transformation initiative, will also decrease operating costs, enabling insurance companies to increase their profitability and offer their customers more competitive premiums.

Read more: How AI Drives Digital Transformation In The Insurance Industry

The Essential Components of Digital Transformation

The technology trend in insurance is clearly moving from the strictly paper-based methods of the past to the digital. Beyond static websites to mobile apps. Beyond email to text and chat. Beyond processes driven by people to more and more intelligent automation that speeds up and uniformly handles all kinds of processes from marketing, and operations, to customer service.

Every organization’s digital transformation roadmap should be as unique as the business itself, but every digital transformation strategy must include a few core elements:

- Clear objectives

- An integrated plan

- A leadership-driven approach

- Investments in the right technology

When creating your organization’s digital transformation strategy, you should start by defining your “why.” In other words, you must identify the reasons you are undertaking this initiative in the first place.

From there, work with a digital transformation partner who can help you create an integrated plan that includes everyone from executive members to line-level employees.

Digital transformation efforts — even small ones — require the active support of top management. Change is the hardest thing to achieve in the organization and without the sponsorship of the corporate leaders, the effort is unlikely to succeed.

Finally, you will need to replace outdated, inefficient technology with modern, robust solutions. When appropriate,

partner with a custom software development firm that can provide you with a purpose-built solution you need for your business. They are equipped with the personnel and experience to generate a solution in the minimum timeframe and without the need to increase in-house headcounts.

If your organization has been exploring ways to improve the customer service experience, increase productivity, improve profitability, and streamline its operations, it is more than ready to embrace digital transformation.

Successfully facilitating digital transformation requires a cohesive strategy, some cutting-edge technologies, a commitment to doing things better, and the right development approach.

Read more: Digital Twin Improving Predictability and Risk Management in Insurance!

How Fingent Can Accelerate Your Process

Naturally, the cornerstone of any digital transformation initiative is technology choices. These may be an off-the-shelf system for standard processes, the integration of existing systems or, your transformation may demand a custom solution that can accommodate your business needs unlike systems available to anyone else.

At Fingent, we specialize in creating resilient custom software solutions that are able to change and adapt according to your requirements. We work with insurance industry clients to help them streamline mission-critical business processes, and – as in all our projects – we accomplish this by providing dynamic, unique software that incorporates the most appropriate technology, such as the latest in machine learning and artificial intelligence technologies.

Connect with Fingent today to accelerate your digital transformation with the help of an experienced software development partner.

Stay up to date on what's new

About the Author

Featured Blogs

Stay up to date on

what's new

Talk To Our Experts

Overcoming Data Challenges in Insurance: How Blockchain Helps

We live at a time when the global data regulators are increasing their data security requirements across businesses and industry verticals. Data being the most powerful asset of insurance providers, insurance companies worldwide have started implementing steps to secure confidential and sensitive information with the help of advanced technologies like blockchain. The vast growing data holds an immense potential to transform insurance companies, but managing the data coming from multiple sources throws up a lot of challenges. Here’s how blockchain helps in overcoming the data challenges in the insurance industry.

Data Challenges in Insurance Vertical

As you know, insurance is a data-centric service. Let it be life and annuity, property and casualty, risk, loss, or claims, insurers are dependent on large volumes of data for various workflows and operations. With increased data flow comes high risks associated with data storage. A wide range of mobile-friendly options is now made available for consumers by the insurance providers to share their personal data. When insurers request access to customer-specific information, they must ensure the authenticity and security of the data collected. The rapid adoption of digital transactions has left insurers in a complex situation to identify new ways to streamline processes and secure sensitive information.

A recent report from McKinsey states that an estimated 5 to 10 percent of all claims are fraudulent, which costs the US-based non-health insurers more than USD 40 billion per year. Besides handling huge amounts of data, the insurance industry struggles with complex compliance issues, third-party payment transaction challenges, slow growth in matured markets, and fraudulent claims activity. Insurers can overcome these obstacles by gaining more accountability, transparency and superior security provided by the blockchain tech.

Related Reading: Top Five Barriers To Growth and Adoption Of Virtual Customers

How Blockchain Rescues Insurance Companies

For an insurance provider to capitalize on the large volumes of data generated, the data must be analyzed in depth to derive useful insights. This process first requires the data to be stored in a trusted manner. Blockchain allows an action to be performed using a predetermined set of rules that are based on threshold triggers in the data. This huge potential of blockchain plays a major role in saving cost and time as well as increasing your business value.

Blockchain makes use of advanced cryptographic techniques, also known as distributed ledgers, to store data. A secure ledger of data is created which cannot be modified, added, or removed without proper authorization. The advantage of Blockchain that is leveraged by the insurance industry over other technologies is the data security it offers along with clear audit trails. The data stored in a blockchain is immutable as it resides in a distributed ledger that executes transactions using a consensus-based mechanism. Each action is recorded permanently with a time and date stamp, such as titles or document histories, which improves the storage’s credibility.

Securing Insurance Data

Blockchain offers the following capabilities to handle data challenges in the insurance industry:

1. Distributed Network – Every participant in the blockchain network has a full copy of the ledger. This ensures transparency among all those who’re part of the insurance workflow.

2. Programmable Network – Blockchain is programmable with the use of smart contracts, also known as crypto contracts. These are programs that control the transfer of digital currencies and assets between parties directly. They also execute transactions and simplify repetitive processes with real-time auditing and assessment of risks.

3. Time-stamped Transactions – Transaction timestamps are recorded in a block which ensures no data is corrupted/ tampered.

4. Secure – Records are individually encrypted and cannot be manipulated.

5. Irreversible – Validated records are immutable, that is, they cannot be changed.

6. Anonymous/ Pseudonymous Identity – The identity of participants is either anonymous or pseudonymous, which ensures the confidentiality of customer data.

Related Reading: How AI and Machine Learning are Driving Cyber Security in FinTech?

The Upcoming Trends

Decentralized validation, redundancy (continuous replication of data), immutable storage, and encryption are the most important characteristics of blockchain that make it a viable option for insurance companies. Through decentralization, it enables faster and cost-effective peer-to-peer transactions, compared to the traditional methods.

Blockchain is expected to open new channels into different market segments and geographies. The Insurance industry is taking leaps and bounds to explore the many advantages of blockchain technology. An industry-wide collaboration among market players, technology evangelists, start-ups, and regulators can help create more potential use cases of blockchain in insurance, leading to operational transformations in a better regulatory environment. Just as the early bird catches the worm, getting involved in partnerships and industry changes at the earliest is key to shaping the future of the blockchain-insurance ecosystem.

Whether you need a detailed/crisp briefing on Blockchain and how the technology can add value to your insurance business, give us a call asap. Our custom software development expert will guide you on how to take advantage of blockchain in your business.

Stay up to date on what's new

About the Author

Featured Blogs

Stay up to date on

what's new

Talk To Our Experts

Robotic Process Automation Reflecting The Banking, Insurance & Logistics Industries

Robotic Process Automation is the fastest-growing segment of the global software market. Using this technology, companies can fast-track their digital transformation initiatives. Although RPA is useful in all industries, the biggest adopters of this technology are banks, insurance companies, and logistics. These companies traditionally have numerous legacy systems and choose RPA solutions to enhance or replace manual IT processes. This article discusses how Robotic Process Automation is revolutionizing the banking, insurance, and logistics industries. First, let’s consider what is Robotic Process Automation.

What is Robotic Process Automation?

Robots have fascinated humans for a very long time. From the futuristic robot Maria from the movie Metropolis in 1927 to this day of AI sci-fi, the possibility with robots is a topic of endless discussion. Interestingly, though, this word “robot” in Robotic Process Automation (RPA) does not involve a physical or mechanical robot. Instead, it is a software running on a virtual or physical machine. Aaron Bultman, director of Product at Nintex simplified the expression saying, “RPA is a form of business process automation that allows anyone to define a set of instructions for a robot or ‘bot’ to perform.”

How to accelerate your business growth with Robotic Process Automation

According to Gartner, RPA grew by 63% in 2018 and continues to be one of the fast-growing technologies in many industries! RPA lets companies automate current tasks as if a real person was doing them across systems and applications. It interacts with each system just as a human user would interact. This does not require complex system integration. These functional RPAs are virtual workers and execute rule-based information processes, enhancing efficiency and accuracy. Additionally, it is easy to model and deploy. Let us consider the three specific industries where RPA is most beneficial.

RPA in Banking

The banking industry is completely process-oriented. Every activity is done meticulously to avoid errors in processing. The repetitive nature of the job and the high probability of human error could cause mistakes that might prove very costly. Therefore, in the recent past, leading banking institutions have started using RPA to minimize errors. According to a report by KPMG, RPA will perform almost 75% of the existing offshore jobs, which could save operational cost.

Scalable Benefits of RPA in the Banking Industry

- Mortgage Lending. RPA can enable the banking industry to meet loan quality and cost concerns head-on. Automation of repetitive and time-consuming manual tasks will free up your team to focus on the more important details of loan applications. It speeds up the work, increases revenue. enhances customer experience, reduces operational costs, decreases risk and improves compliance.

- Compliance and Risk Management. It enables the banking industry to automatically integrate and aggregate compliance information into business processes, streamlining the required work while reducing expenses. RPA eliminates the need for manual regulatory monitoring and data collection. It can empower risk management and compliance teams. It enables banking industries to avoid costly fines and damages to reputation. It provides accurate and complete information.

- Customer Service and Support. RPA ensures the longevity and loyalty of your customer relationship and the future of your bank. It helps you engage customers in real-time. It automates customer service activities so the customer is not waiting endlessly. It increases the productivity and efficiency of the team.

Related Reading: Check out these 5 simple hacks on using banking mobile apps safely.

RPA in Insurance

An insurance company receives hundreds of claim requests. Validating each request and handling them is not only a herculean task but also a painstakingly slow manual process. The entire process of the claim takes several days. Because this is a costly and time-consuming process, the company risks losing customers. To prevent further damages, insurance companies are now relying on RPA to help them improve operational excellence and reduce costs.

Scalable Benefits of RPA in the Insurance Industry

- Improves customer service because RPA effectively reduces the turnaround time in resolving customer issues.

- Processes and workflows could be tracked and recorded at each phase. This reduces staff workloads and improves process efficiency.

- Reduces the processing time by 40-80%. This frees up the team to focus on more important activities such as acquiring new clients.

- Reduces errors made during data entry significantly.

- Speeds up and organizes the processing of claims through a systematic underwriting process.

- Based on the demand, intelligent bots can scale up or down, which delivers consistency in service and operational efficiencies.

- Improves audibility and operational risk management due to the accuracy level of RPA.

- The time for the cancellation process could be reduced by one-third.

Related Reading: Here’s how machine learning is accelerating paperless offices for legal firms.

RPA in Logistics

The logistics industry depends on several processes to facilitate the proper distribution of products, materials, and services from B2B or B2C. The need for an intelligent logistics system increases as the industry along with competition advances every day. Here’s how the RPA can contribute to the logistics industry:

Scalable Benefits of RPA in Logistics.

- Better data management and customer service. Negative experiences and a multitude of errors with logistics providers are causing customers to lose their trust in online shopping. With the benefits of automation and digitalization brought about by RPA, logistics providers no-longer need to rely on huge amounts of paperwork, which was the underlying cause for errors and poor customer service. Logistics companies are enabled to manage real-time monitoring of flow and resources, availability, costs, staffing, transportation, suppliers and so on more efficiently.

- Improved work safety for employees. Through the use of automated machines in unsafe environments and the reduction of repetitive stress in manual tasks, work injury has been dropping steadily with the aid of RPA. This results in savings in terms of injury compensation and loss in reputation. It can also increase productivity, improve employee satisfaction and loyalty, and increase their efficiency.

- Improved efficiency and precision. RPA can help logistics companies easily manage the supply chain processes more efficiently. The anticipatory logistics system helps companies gauge the demand from their customers and adjust their production volume accordingly. It can help in managing and analyzing huge amounts of data within seconds, resulting in fewer human errors, faster deliveries, and fewer errors in delivery.

- Cost reduction. Fewer errors from human decision-making result in cost savings for logistics companies. Also, RPA reduces the need for human workers, which results in fewer paychecks and more profits. Where workers are still needed, it can raise their productivity, margins to a whole new level. It improves customer satisfaction and creates a safer work environment for the workers.

Related Reading: Know more about how AI is reshaping the supply chain and logistics industry.

Empower Your Business With RPA

According to Global Market Insights Inc., the RPA market is expected to reach $5 billion by 2024. It is increasing capabilities and improving performance while reducing costs in several industries. Fingent Technologies has been one of the top software companies empowering industries globally with robotic process automation capabilities. Give us a call and let us discuss how we can transform your business with RPA.

Stay up to date on what's new

About the Author

Featured Blogs

Stay up to date on

what's new

Talk To Our Experts

How Machine Learning Edges Us Closer to Paperless Office?

Paper! Paper! Everywhere! Until recently you couldn’t imagine an office without paper. But today, Machine Learning allows you to print, sign, fill and scan digitally. It eliminates the hassle of handling multiple paper documents and helps organizations in converting to a paperless office.

In this blog, we will discuss how ML is influencing the modern workplace, the importance of paperless office and the industries which are seeing a tremendous impact through paperless technology.

The Role of ML in Achieving a Paperless Workplace

Machine Learning (ML) which is a subset of Artificial Intelligence (AI), is a science of software application where the program can learn to provide accurate outcomes without detailed coding. Through reinforcement signals, the software is able to “learn” the best possible approach to achieve the desired goal. Machine Learning algorithms are being trained to take on collaborative business processes and workflows for automation. This enables employees and the organization to go digital.

Machine Learning replaces huge filing cabinets and the laborious process of searching for the right information. To find information easily, to collaborate and manage a business more effectively, ML uses powerful search and discovery tools. Since computers have the ability to process calculations, scan large amounts of data, and assess probabilities in a matter of seconds, Machine Language (ML) is proving to be an extraordinary innovation that will greatly impact the workplace. Let us consider some aspects of office organization and how ML is superior to the traditional paper workflow.

Related Reading: AI and ML are revolutionizing software development. Here’s how!

-

Efficient Document Organization

You save time in searching for documents. Information is readily accessible to all employees. Restricting access to confidential documents is made easier. You could access digital documents from anywhere which facilitates remote working. The origin of digital documents can also be traced easily.

-

Enhanced Security

Customers are often concerned about data protection. This requires that companies provide greater security beyond paper shredders and locked filing cabinets. The digital format offers greater document security. Since it is inexpensive to create backups, it is easier to retrieve lost or stolen data.

-

Lower Overhead Costs

Research estimates that an office worker makes more than 60 trips per week to the printer, fax machine, and copier. Digitizing documents eliminates those trips as well as the need to buy expensive equipment and pay for their maintenance. This has a direct impact on reducing operating costs. Digital documents could be sent across by electronic mail, saving postal costs.

-

Lesser Storage Space

A paperless office software frees up space. Companies now can archive everything on private company servers or in the cloud. Jonathan Velline, executive vice president for ATM banking and store strategy at Wells Fargo, talks about the benefits achieved by utilizing paperless document management tools and wireless devices: “It’s a very efficient use of space for us. In a 3,000 square-foot store, we would have an area for full-service banking and a separate area for self-service banking. Here we fit it all in one place.” Having a fully integrated paperless system, employees don’t have to have designated offices. Mini work areas inside the store are more than enough to digitally access customer information and any other details required. This way, Wells Fargo, reduced their office space to three times smaller than the average location.

Related Reading: You may also like to take a look at the top AI trends of the year!

How has Machine Learning Helped Industries to Go Paperless?

Machine Learning has found application in many industries and has helped them in going paperless. Let’s consider three such formerly paper-heavy sectors – legal firms, the automobile industry, and the insurance sector:

Legal firms

ML facilitates greater efficiency and productivity by allowing a lawyer to shift his focus from labor-intensive tasks to core functions like counseling, analysis, and advocacy. Since it is capable of eliminating the laborious process of managing and reviewing boilerplate documents within legal contracts, it allows time for attorneys to appear in court, advice their clients, and negotiate deals. ML can also generate alerts to provide advance notification regarding crucial dates in contracts, such as renewal dates. It can reduce the overall cost of litigation in many ways. It reduces the amount of time a lawyer spends on proofing a document and helps locate relevant information quickly. Use of computer algorithms also helps an attorney identify relevant information that is buried in electronic documents. ML is further equipped to provide a paper-free trial for legal firms.

Automobile industries

Machine Learning enables machines and devices to replicate the way humans learn. This has enabled great strides in the automobile industry in terms of supporting a paperless office. Machine Learning is also capable of generating highly sensitive autonomous systems that can speed up the process of filing claims if an accident occurs, eliminating the time consuming and paper-heavy process of filling up elaborate forms.

With ML algorithms, the automotive industry is set to have various features like automatic braking, pedestrian, collision avoidance systems, and cyclists’ alerts. It also supports dealers and manufacturers by enabling a paperless update of the vehicle’s firmware. Through the cloud, a diagnostic system can communicate any problems by sending performance data directly to the manufacturer or schedule repairs.

Insurance

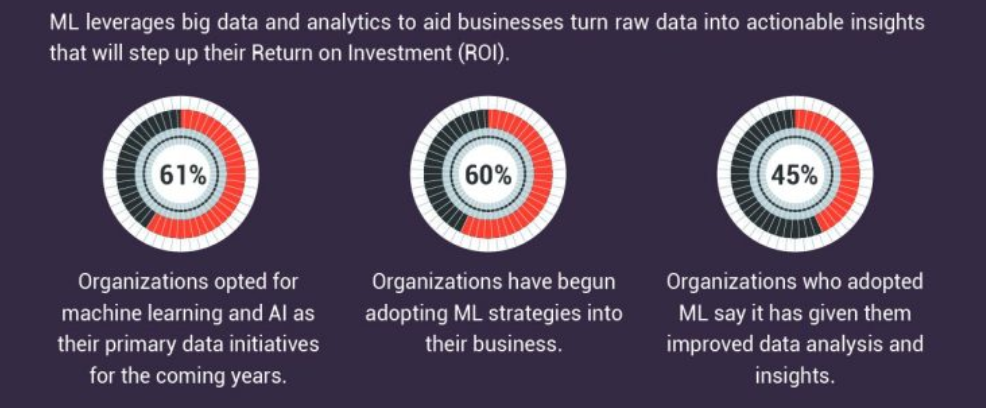

Insurers are using Machine Learning to boost customer service, increase their operational efficiency, and even detect fraud. ML can improve the process of insurance and automatically move claims through the system. With sophisticated rating algorithms, companies are able to fit in most risks as long as they find good pricing. ML can support agents in classifying risks and calculating accurate predictive pricing models. Tools powered by ML, help consolidate volumes of highly varied data such as membership and provider data, insurance claims data, benefits, and medical records without the use of paper. These solutions can process and structure data with insights leading to a higher quality of care, costs reduction, and fraud detection.

Insurers can draw insights from data about behaviors, individual preferences, lifestyle details, attitudes, and hobbies to create personalized products such as loyalty programs, policies, and recommendations.

Machine Learning- Deciphering the most Disruptive Innovation : INFOGRAPHIC

Go Paperless Now!

The call to move to a paperless office is getting more urgent every day. To make this transition easy, we can help your organization reap the best benefits of Machine Learning. Give us a call and let’s talk!

Stay up to date on what's new

About the Author

Featured Blogs

Stay up to date on

what's new